Tax Issues Related to Enterprise Cancellation

|

Q: |

Before applying tax cancellation, what should the taxpayers (enterprises) do? |

||||

|

A: |

Taxpayers should complete the tax clearance for tax payable, tax refund, late payment surcharge and fines, the cancellation of invoices and other tax documents before applying tax cancellation, including:

|

||||

|

Q: |

What are the conditions for immediate processing of tax cancellation? |

||||

|

A: |

Taxpayers who have not handled tax-related matters and take the initiative to go to the tax authority for tax clearance, the tax authority may issue tax clearance documents based on the business license provided by the taxpayers immediately.

While taxpayers who have been declared bankrupt by the court, can bring the “Ruling of the Court on the Termination of Bankruptcy Proceedings” to apply to tax authorities for tax cancellation, the tax authority shall issue a tax clearance document immediately. The taxpayers who meet the following conditions when they apply tax cancellation, the tax authorities provide immediate settlement services, adopt a "commitment system" and issue tax clearance documents immediately:

|

||||

|

Q: |

What documents need to be provided when enterprises apply to the tax authorities for tax cancellation? |

||||

|

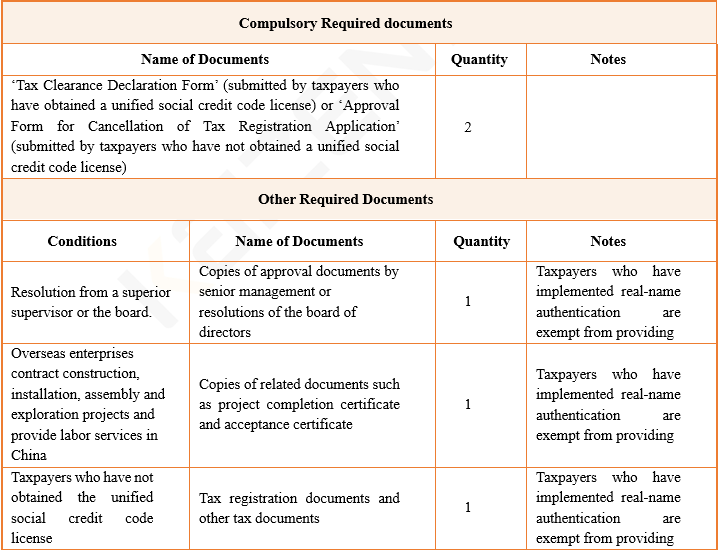

A: |

The enterprises apply to the tax authority for tax cancellation, below materials and documents need to be provided:

|

||||

|

Q: |

After the taxpayers complete the tax cancellation, and obtains the cancellation notification, how to cancel the third-party payment agreement between the bank and tax authority? |

||||

|

A: |

Taxpayers who complete the tax cancellation, do not need to propose to the tax authorities for the termination of third-party payment agreement between bank and tax authority. After the tax authority completes the tax cancellation, the third-party payment agreement between the bank and tax authority is automatically terminated.

|

Language

close